As we exit summer and head into fall, it is easy to be fooled that we have things moving back to a bit of normality. Children are starting school, family schedules are filled with sporting events and youth activities and we are getting back to our normal routines. However, in quiet corners and hushed tones at parties and events, people continue to ask, “What in the world is going on?” Everyone is trying to make sense of the political instability in the US, the war in Ukraine, saber-rattling with China and Taiwan, and the continued economic malaise that we all feel daily. A recent New York Post survey shows 74% of Americans believe the US is on the wrong track and this will make for an interesting upcoming election cycle. I get the sense that people are tired, frustrated, and doing everything to force themselves back into a state of normal when we are in anything but that state.

To add further insecurity, American consumer debt is increasing with rising delinquencies. The DOW is down 17.3% year to date with a consumer price index in June of 9.1%, 8.5% in July, and 7.9% in August. Most realize that the Federal Reserve and other experts were wrong when they told the public that inflation would be “transitory.” Since 2009 governments worldwide have printed over $35 trillion that was injected into the economy. We are having a hard time understanding what “real” supply and demand for any asset is, and thus it’s real price for those assets worldwide.

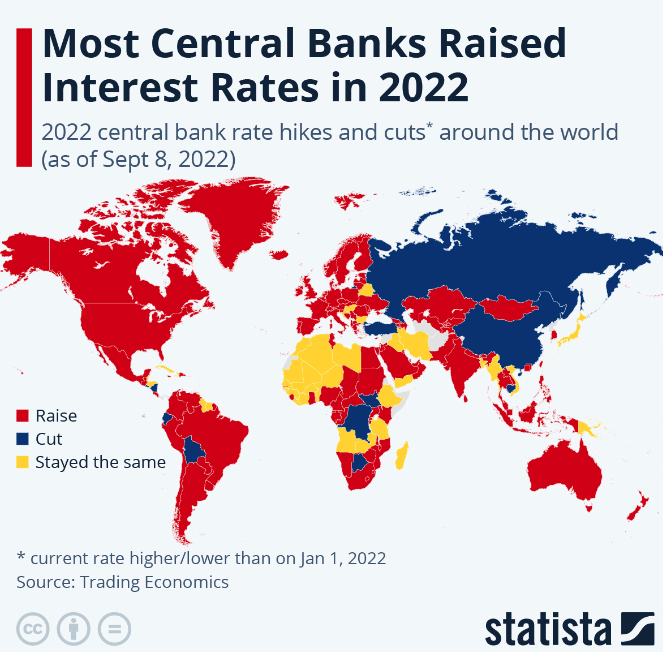

Fundamentally, there are two ways to slow inflation; decrease demand or increase supply. Traditionally, the Federal Reserve would raise interest rates to make money for expensive and thus slow demand. Increasing demand usually fell to the private sector to grow the economy with massive capital expense (CAPEX) investment and spending to improve operations, business, etc. The private sector did this in the 1970’s and major inventions and engineering feats helped the US and others in the global economy grow out of a bad economy. Analysts who study this today are concerned that we don’t see these types of long-range CAPEX investments in the private sector.

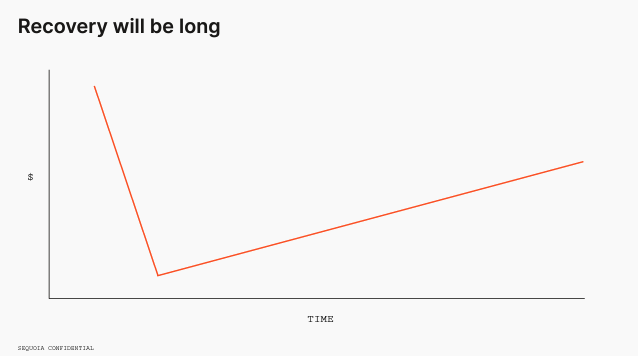

The current administration is not helping fix supply or demand in the United States but rather throwing gas on the fire by increasing demand by providing tax holidays and sending stimulus checks to American families. Although offering short-term relief, this will draw out the economic malaise we find ourselves in. For those hoping things would economically get back to normal this fall, we have longer to wait. After the Great Financial Crisis of 2008, it took a full four years to work everything out. This time it will be longer with $35 trillion to work out of the economy. We have a bumpy road ahead.

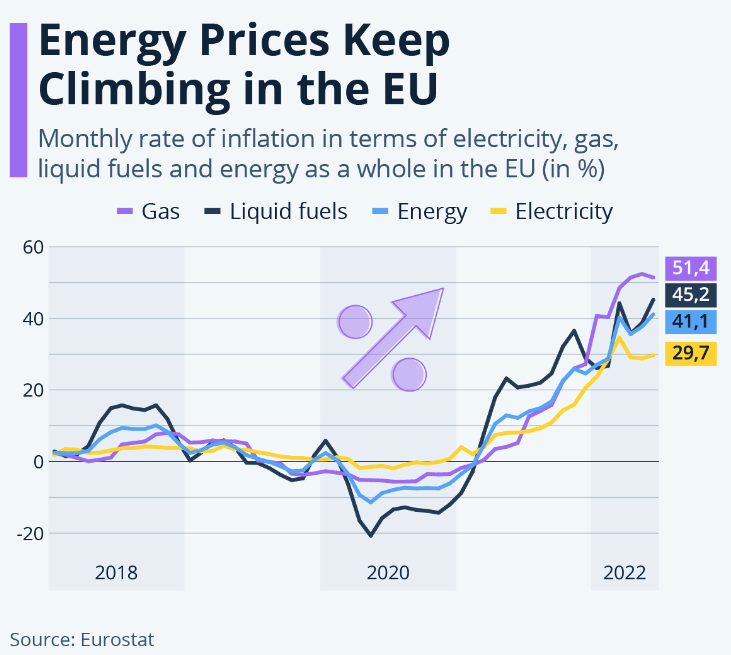

This, of course, was predicted by many from former Secretary of the Treasury Larry Summers and President Trump who warned Europe of the precarious position they were in giving Russia so much leverage over them and their economy. Europe is dependent on Russia’s natural gas for over 45% of all their energy needs to heat their homes and fuel their factories and industry.

President Trump was laughed off the stage at the UN in 2018 when he told them they needed to be energy independent. (See the graphic above and the price of energy in Europe in 2018 compared to today.) A crisis of epic proportions is now brewing in Europe heading into the winter. French nuclear reactors were at reduced capacity most of the summer, hydroelectric facilities the same due to drought conditions, and Germany is now firing up its coal plants and importing natural gas as fast as possible to head off an economic and social disaster heading into the winter.

Meanwhile, Vladimir Putin just played his best hand having Gazprom turn off Nord Stream 1 for “operational issues” to show all of Europe just how much leverage he has over them. Winter is coming and the pain is going to get a lot worse. This is a gun to the head of all of Europe. Not only will economies falter, inflation will rise, but people will starve and freeze to death in the streets of capitals all over Europe unless something is done. Riots are already taking place in capitals around the EU. The people will demand a resolution to the war in Ukraine and most experts believe that with this pressure, a deal will be found soon. Germany is my pick to break first to seek a resolution. All the while, Russia has continued to sell its oil and natural gas around the sanctions and its economy and currency have actually been doing quite well all things considered. EU leaders are waking up that the energy plan for Europe was not feasible and modifications need to be made.

Ideas have consequences. The Environmental, Social, Governance (ESG) movement has aspects that all good stewards of the planet can agree on, however the method of implementation and speed at which this has been adopted has had serious consequences we are just now beginning to understand. These are laid bare for all to see. Large transitions like this need nuanced discussion and well-thought-out plans. Even green energy advocate Elon Musk has warned that the world needed to rely on nuclear and fossil energy while making an orderly transition to all ESG goals. Europe willingly rushed to go “carbon neutral” while shutting down clean energy nuclear power plants and still being reliant on 60% of its energy being imported and mostly from Russia put them at the mercy of Russian cooperation. Sri Lanka on the other hand was forced to adopt ESG standards to obtain funding from the World Bank and the IMF. It’s near perfect 98% ESG rating is incredible compared to the United States barely hitting 50%. To achieve these great results, Sri Lanka outlawed fertilizer and pesticides for its farmers and agriculture, along with many other measures. Their crop yields are down dramatically for rice and agriculture pushing their country to the brink. People are starving and there have been riots in the streets forcing the President to flee to the Maldives. This is just the beginning of turmoil. With their government and economy failing investors will start to pull out impacting them further. Sri Lanka could be just the start of many emerging economies that start to fail; the domino effect could quickly take others down. This is a contagion that will not be easy to stop.

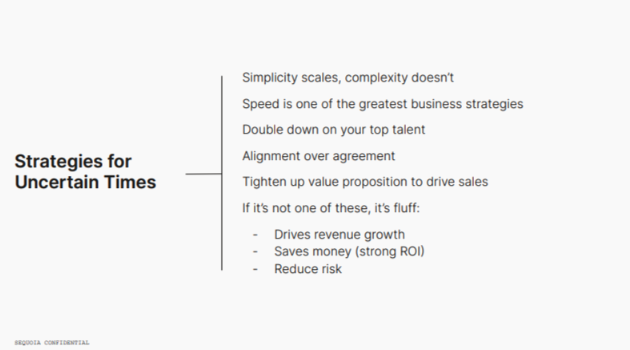

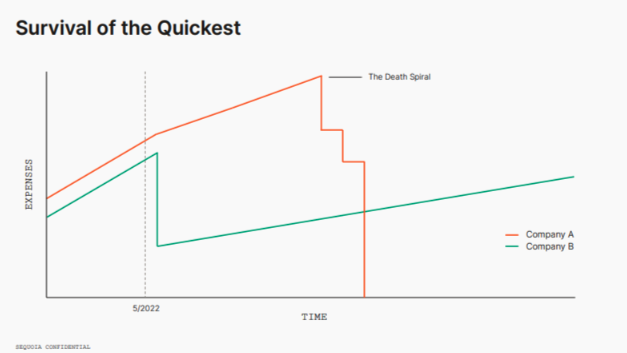

This is not a time for naval gazing for nation-states, companies, or people navigating these interesting times. We need to understand the times and take intentional action towards a goal. We all know that action is faster than reaction and in the military, we are taught to “always be improving your fighting position.” The same rules apply in life. Whether you are running a business, managing your home and personal finances, or planning your career, there are steps that everyone needs to take to be prepared. A fact of life is that everyone must organize and plan their life with a different set of rules. Those who know the game has changed and pivot and adapt quickly will not only survive but thrive. Sequoia Capital recently to the founders of the companies they invested in and said this is a time for “Survival of the Quickest” and I could not agree more. Their assessment is a must-read for business leaders and employees alike. (Link to 56-page Sequoia “RIP Good Times” Presentation.)

Over the last decade of cheap capital, many companies were able to survive and grow top-line revenue due to access to cheap debt and abundant financing and investment rounds. Some were able to do this with total disregard to the bottom line and profitability and even cheered on by the stock market as valuations soared. Those days are over. Top line growth at all costs while burning capital to obtain market share with disregard for bottom line profitability is over in this climate. Those who have built businesses and focused on the fundaments, been cost-conscious, managed finances well, have a strong balance sheet, and run profitable cash-flowing businesses will be in high demand. It’s a different mindset and skill set to grow a profitable company without abundant investor capital to burn. The entrepreneur that has grown the skill sets to be frugal, resilient, and bootstrapping in a capital-restrained environment understanding how to cut expenses while growing a cash-flowing profitable business will have an edge in this environment.

For non-business owners who are managing their finances and balancing personal or family budgets, these principles will also be applicable to you. To start, I am reminded of the old saying, “If you are going to cut the dog’s tail, don’t do it an inch at a time.” Everyone should be looking at making cuts to expenses. Don’t do it a bit here and there over time. Most business leaders will tell you their only regret on making cuts is that they did not do it sooner.

My recommendation is to build a budget and make drastic cuts to expenses all at once. Don’t wait hoping things will get better. You will be glad you went through this exercise and you can always add back things later if you need to. The key is to get as much margin in your monthly budget as possible. If you are living with little to no margin, you probably have already seen inflation close that gap to nothing. Rising credit card debt in the United States indicates many families are closing this margin gap with this. This is a bad short and long-term solution. Understanding your budget and making cuts is critical to your financial health. The next step will be finding new revenue streams to grow your income. The great news is that the gig economy is growing and thriving like never before, so there are many options to add new profit centers and revenue to your monthly budget.

1 Comment

Leave a Comment

My Books:

Get my latest book Love Your Work: 4 Practical Ways You Can Pivot to Your Best Career

Whether you’re just starting out, looking for a change, or experiencing unwanted change, there’s a way forward. Love Your Work is about pivoting step-by-step to a more satisfying career.

Get The Leap: Launching Your Full-Time Career in Our Part-Time Economy

Long-term careers are on the way out, and "gigs"-part-time, contract, or freelance work-are becoming more common.

Whether you're in the midst of a career or just getting started, now is the time to prepare for changes headed your way.

Order my book, The Leap, today!

I am so happy I found this article who can put to paper what I am thinking a little about. Until I read this I thought I had thought a LOT. He nails it. Don’t scan it…read it!